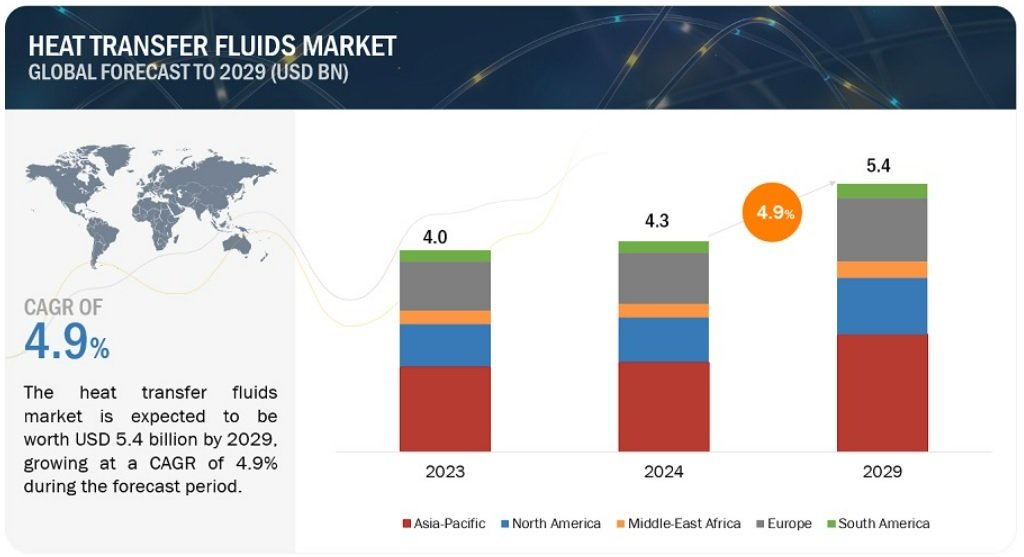

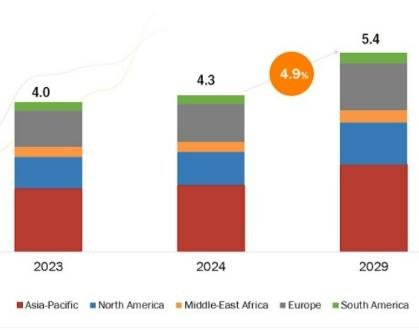

The report “Heat Transfer Fluids Market by Product Type (Mineral Oils, Synthetic Fluids, Glycol-Based Fluids), End-use Industry (Chemical & Petrochemicals, Oil & Gas, Automotive, Food & Beverages, Pharmaceuticals, HVAC, Renewable Energy) – Global Forecast to 2029”, is USD 4.3 billion in 2024 and is projected to reach USD 5.4 billion by 2029, at a CAGR of 4.9%.

The growth of the heat transfer fluids market is driven by several key factors, including rapid industrialization, increasing demand for energy efficiency, and the expansion of key end-use industries. As industrial processes become more advanced and widespread, particularly in emerging economies, the need for effective thermal management solutions becomes critical. Industries such as chemical and petrochemical, automotive, food and beverages, and HVAC heavily rely on heat transfer fluids to maintain optimal operating temperatures and ensure process efficiency. The growing emphasis on energy conservation and efficiency further propels the market, as heat transfer fluids are essential in reducing energy consumption and improving the overall efficiency of thermal systems. Additionally, the rising adoption of renewable energy sources, such as solar and wind power, necessitates advanced heat transfer fluids for energy storage and transfer applications. Technological advancements and innovations in heat transfer fluid formulations, offering better thermal stability, lower maintenance, and higher operational safety, also contribute to market growth. Furthermore, stringent environmental regulations and the push towards sustainable industrial practices encourage the use of high-performance, environmentally friendly heat transfer fluids, thereby driving market expansion. These combined factors create a robust demand for heat transfer fluids across various sectors, fuelling the market’s growth.

Mineral oils by product type are projected to be the largest, in terms of value, during the forecast period

Mineral oils hold the largest market share in the heat transfer fluids market due to their cost-effectiveness, availability, and performance characteristics. Significantly cheaper than synthetic and glycol-based fluids, mineral oils’ low production and refining costs make them an attractive option for industries optimizing their budgets. Derived from abundantly available crude oil, mineral oils benefit from a well-established global supply chain, ensuring a steady supply and reducing the risk of shortages. They offer a good balance of thermal stability, heat transfer efficiency, and operating temperature range, making them suitable for chemicals, petrochemicals, and manufacturing sectors. Their ability to maintain consistent performance under varying thermal conditions ensures reliable and efficient heat transfer systems. Additionally, mineral oils’ versatility allows for use in a wide range of applications, simplifying maintenance and inventory management. Compatibility with most materials in heat transfer systems reduces corrosion risk and extends equipment lifespan, further enhancing their economic appeal. Consequently, these combined advantages secure mineral oils’ leading position in the heat transfer fluids market.

Chemical & Petrochemicals by end-use industry is projected to be the largest, in terms of value, during the forecast period

The chemical and petrochemicals end-use industry holds the largest market share in the heat transfer fluids market due to its continuous demand for efficient thermal management. This sector involves processes like distillation, polymerization, and chemical synthesis, requiring precise temperature control essential for producing a wide array of chemicals. Heat transfer fluids maintain optimal reaction conditions, ensure process safety, and enhance energy efficiency. The large scale and complexity of petrochemical operations necessitate significant volumes of heat transfer fluids to manage substantial heat loads. Stringent requirements for operational reliability and safety favor high-quality fluids that withstand harsh conditions and offer long-term stability. The sector’s continuous growth, driven by rising global demand for chemicals and materials, reinforces its dominance in the market. This growth is particularly significant in regions with substantial chemical production capacities, such as North America, Europe, and Asia-Pacific, further solidifying the chemical and petrochemical industry’s leading market position.

Asia Pacific is expected to be the fastest growing market for heat transfer fluids during the forecast period, in terms of value

Asia Pacific leads the heat transfer fluids market due to rapid industrialization, strong economic growth, and the presence of major end-use industries. The region’s booming chemical and petrochemical sectors, especially in China, India, and Japan, generate significant demand for heat transfer fluids necessary for distillation, polymerization, and chemical synthesis processes. Additionally, the expanding manufacturing base in Asia Pacific, encompassing automotive, electronics, and food and beverage industries, further drives the need for efficient thermal management solutions. Rapid urbanization and infrastructure development also increase demand for HVAC systems, where heat transfer fluids are crucial. The push for renewable energy sources like solar and wind power in countries such as China and India fuel the need for these fluids in energy storage and transfer applications. Favourable government policies, industrial project investments, and raw material availability support the market’s growth. These factors collectively position Asia Pacific as the largest and fastest-growing region in the global heat transfer fluids market, surpassing Europe, North America, South America, and the Middle East & Africa.

Key Players:

The key players in this market are Dow (US), Eastman Chemical Company (US), ExxonMobil (US), Chevron Corporation (US), Huntsman Corporation (US), Shell PLC (UK), Lanxess (Germany), Clariant (Switzerland), Wacker Chemie AG (Germany), Indian Oil Corporation Ltd. (India), Schultz Canada Chemicals Ltd. (Canada) etc.