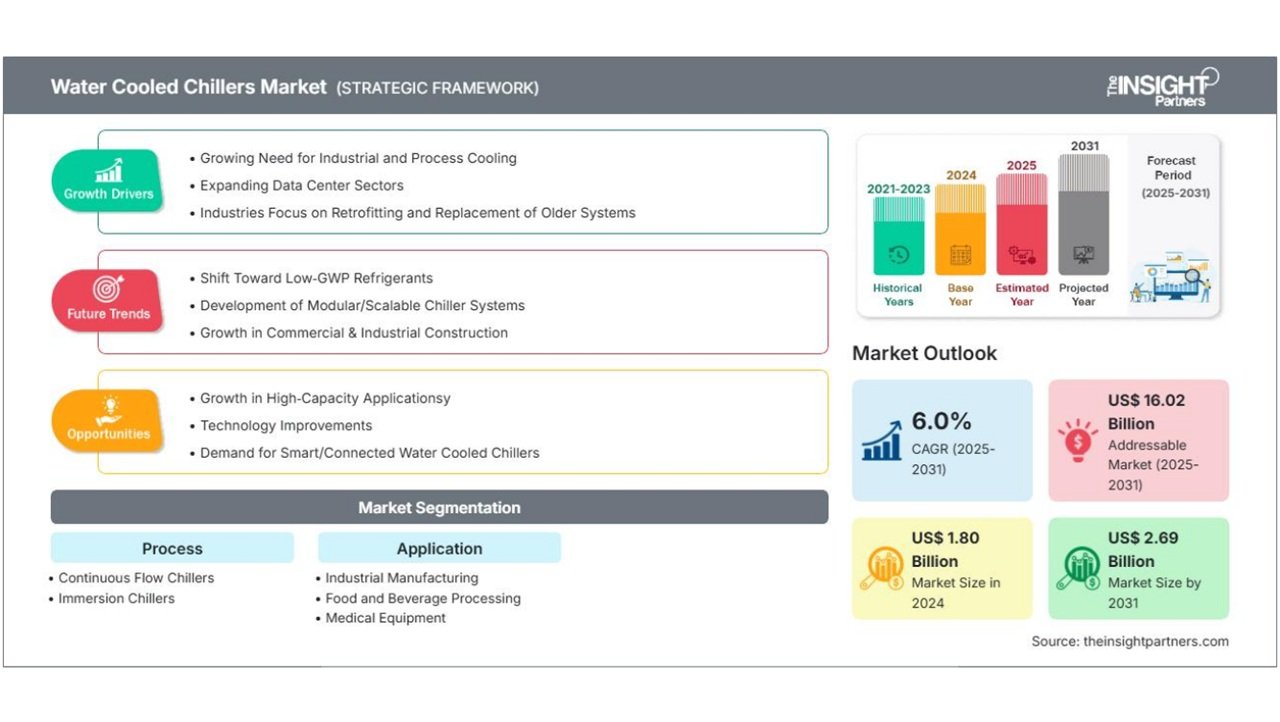

The global market for water-cooled chillers is projected to grow from US$1.80 billion in 2024 to US$2.69 billion by 2031, according to a new report by The Insight Partners. This represents a compound annual growth rate (CAGR) of 6.0% from 2025 to 2031, driven by rising demand for industrial and process cooling, retrofitting of older systems, and the expansion of data centers.

The report highlights strong adoption of continuous flow chillers across industrial manufacturing, food and beverage processing, and medical equipment sectors. Future growth is expected in smart and connected chillers, high-capacity applications, and improved system efficiency.

The growing use of artificial intelligence, cloud computing, and big data analytics has increased heat loads in data centers, requiring advanced cooling solutions. Water-cooled chillers are noted for their energy efficiency and precise temperature control, making them suitable for such high-demand environments.

In 2024, the Asia Pacific held the largest market share, driven by demand for continuous processing solutions in manufacturing and healthcare. The region is also expected to record the highest CAGR through 2031, supported by growth in commercial construction projects such as airports, malls, and hotels.

By process type, continuous flow chillers led the market in 2024, while the industrial manufacturing segment held the largest share by application. Among system types, chillers used in machine tools accounted for the largest market portion.

Key market players named in the report include Stulz SpA, Mitsubishi Heavy Industries Ltd., Daikin Industries Ltd., Johnson Controls International Plc, Panasonic Holdings Corp., HYDAC International GmbH, Blue Star Ltd., Carrier Global Corp., Trane Technologies Plc, and Thermo Fisher Scientific Inc.

Recent product developments mentioned include Daikin Applied’s launch of the Magnitude WME-D centrifugal chiller using low-GWP refrigerant R-515B, and Johnson Controls’ YORK YVWH heat pump using R-1234ze, introduced in North America.

Read More