For an engineer reading a data center brief in 2026, the first constraint is rarely the heat load. It is whether the site has the electricity, the water, and a use for the rejected heat to run a given cooling scheme at all. The cooling technology, and with it the refrigerant, follows from what the location can supply. This is not a 2026 development. The design and site-selection firm Build.inc dates the shift to around 2023, when GPU racks crossed the point at which cooling could no longer be, in its words, engineered in afterward; the assumption "broke around 2023, and it has not returned" (Build.inc, 2026).

The less examined consequence is what happens next. Once the binding resource sets the cooling architecture, it also narrows the refrigerant. A site that can only reject heat to air in a hot climate, a site whose value depends on selling that heat to a district network, and a site rationing water each point toward different machines, and increasingly toward natural refrigerants such as ammonia (R717), propane (R290), and CO2 (R744). Most current coverage traces the resource constraint as far as the cooling method and stops there, before it reaches the refrigerant.

The demand that forced the question

Global data center capacity is tracked at roughly 103 GW today and is projected to approach 200 GW by 2030 (JLL figures, cited in ATMOsphere's Clean Cooling for Data Centers 2025 report). In the United States, the load is large enough to register at national scale: data centers consumed about 4.4 percent of US electricity in 2023 and are projected to reach between 6.7 and 12 percent by 2028 (US DOE / Lawrence Berkeley National Laboratory, 2024 United States Data Center Energy Usage Report).

The pressure on cooling comes from density. Rack power that sat at 15 to 30 kW has moved to 100 kW and beyond, and air can no longer carry the load economically. Liquid is the obvious answer on physics: water holds close to 3,500 times more heat per unit volume than air and transfers it about 23.5 times faster, which is why direct liquid cooling can cut cooling energy by a fifth or more (Ecolab, 2025). But the move to liquid does not by itself solve the siting problem. It changes which resource binds first.

Compute silicon and electricity are not sequential bottlenecks where one has been solved; they are two parallel shortages. NVIDIA's Blackwell parts are reported sold out into the second half of 2026, and the advanced packaging and high-bandwidth memory behind them are contracted well into 2027. At the same time, infrastructure is slipping: Bloomberg reported in May 2026, drawing on Sightline Climate, that between a third and half of US data centers planned for 2026 are delayed or cancelled, with only about 4 GW of an announced 12 GW under construction. Increasingly it is power, transformers, and switchgear, rather than the chip order, that governs when a facility can open.

Resource one: electricity

The clearest sign that power now leads is the wait to connect. The Lawrence Berkeley National Laboratory's Queued Up: 2025 Edition reports that a typical generation project reaching commercial operation in 2024 spent about five years in the interconnection queue, with the median having doubled over two decades; the active queue stood at roughly 2,290 GW at the end of 2024 (LBNL, 2025). That figure measures generators seeking to join the grid, not data centers seeking load, and the two should not be conflated. For load in the densest hubs, Northern Virginia, Phoenix, and Dallas, reported connection timelines run from four to seven years (Sightline Climate via Bloomberg), with the upper end traced to the Northern Virginia utility Dominion Energy and echoed by the IEA.

The scale of new demand explains the queue. Grid Strategies put five-year US peak-load growth at 166 GW through 2030, of which about 90 GW, roughly 55 percent, is tied to data centers, while the DOE's own figure is near 100 GW with about half attributable to data centers (Grid Strategies, National Load Growth Report 2025; US DOE, 2025). Both organizations caution that utility interconnection requests overstate real demand through double counting.

Operators are not waiting. A growing share are building generation behind the meter, mostly gas: one analysis identifies 46 data centers totalling about 56 GW of planned behind-the-meter capacity, close to 30 percent of the US pipeline, with roughly 90 percent of those projects announced in 2025 alone (Cleanview, reported via Distilled Earth). Goldman Sachs Research expects behind-the-meter systems to supply a quarter to a third of the incremental data center demand to 2030 (Goldman Sachs, 2026). For cooling, on-site generation matters twice: it sets the available power envelope, and it produces its own waste heat alongside the IT load.

Resource two: water

Water has moved from an operating detail to a siting determinant. Direct cooling water consumption by US data centers reached about 66 billion litres, near 17.4 billion gallons, in 2023, and is projected to climb steeply by 2028 (LBNL, 2024, as the primary source; restated in AWWA, 2025, and Environmental Law Institute, 2026). AWWA's Cooling the Cloud projects annual direct consumption rising to between 38 and 73 billion gallons by 2028.

The trade-off is the part engineers cannot design away. Cutting water through air or closed-loop cooling raises electricity use, and generating that electricity itself consumes water upstream. Landon Marston of Virginia Tech estimates that 75 to 90 percent of a data center's total water footprint sits not at the site but in power generation. A facility cannot optimize water and power independently; improving one metric, WUE, often worsens the other, PUE.

Public opposition has hardened around water and land. As of April 2026 there were roughly 69 US states and municipalities with active data center moratoriums, and a Gallup poll in March 2026 found about seven in ten Americans opposed to data centers in their local area, with 48 percent strongly opposed (Gallup, 2026). The financial trace is visible: Data Center Watch recorded 64 billion dollars in US projects blocked or delayed between 2023 and early 2025, then an estimated 98 billion dollars in the second quarter of 2025 alone (Data Center Watch, 2025). Where water permits are the friction point, the cooling design that needs the least water can decide the site, even at a power penalty.

Resource three: heat

Electricity and water are constraints to be managed. Heat is the resource the industry is only now learning to treat as an asset, and the split between Europe and the United States is sharp.

In the European Union, reuse is becoming mandatory rather than optional. The Energy Efficiency Directive requires data centers above 1 MW of IT input to use waste heat or another recovery route unless it is technically or economically unviable. Germany's Energy Efficiency Act goes further with hard numbers: PUE at or below 1.5 by mid-2027 and 1.3 by 2030 for existing sites, 1.2 for sites commissioned from July 2026, and an Energy Reuse Factor rising from 10 percent in 2026 to 20 percent by 2028 (White & Case summary of the German EnEfG, 2024). These targets are in flux; a draft amendment published in April 2026 proposes relaxing the PUE caps after Germany missed an EU implementation deadline (Orrick, 2026). The trajectory holds regardless: in Europe a site's heat now has a buyer, and the cooling system is designed to deliver it at a useful temperature.

In the United States the same heat largely escapes. The behind-the-meter gas build-out is about securing power, not about reuse, and district heating networks that could absorb the heat remain uncommon. The consultancy Cundall has argued that the German act turns waste heat recovery into a national priority and changes how systems are specified, pointing to projects such as the FRANKY scheme in Frankfurt (Cundall, 2026). A mandate to reuse heat favours heat-pump-based architectures and high-temperature lift, where natural-refrigerant systems hold their clearest advantage.

From resource to refrigerant

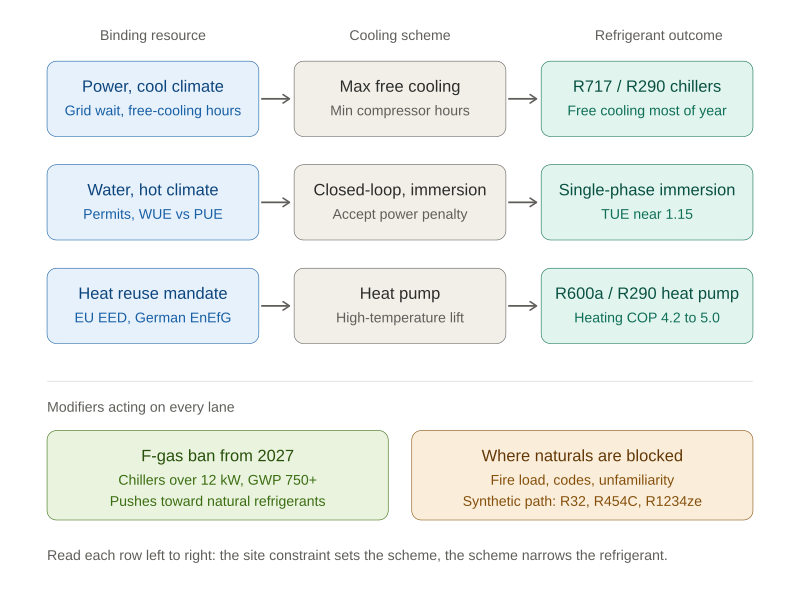

Put the three resources together and a rough decision map appears, and it reaches the refrigerant.

Where power is the constraint and the climate is cool, the design maximizes free cooling and minimizes compressor hours. Natural-refrigerant chillers compete here on efficiency. Zudek reports that an ammonia (R717) chiller replacing an R407C unit ran 2,131 hours a year on free cooling against 195 for the older machine, cut energy use by 43 percent, and saved 185,752 euros a year (ATMOsphere, 2025). In Hamburg, Secon supplied Penta Infra six propane (R290) air-cooled chillers reaching up to 80 percent of annual hours on free cooling with an EER of 4.15 and a PUE target of 1.2 (ATMOsphere, 2025).

Where water is the constraint, the design accepts higher power to avoid evaporative loss, and immersion enters the picture. BAC reports that a single-phase immersion installation at the Skybox Houston One site runs on free cooling year-round even in Houston, with a Total Usage Effectiveness near 1.15 against about 1.60 for an air-cooled chiller with CRAH units, and roughly 80 percent lower cooling energy (BAC, via ATMOsphere). TUE itself is not a vendor metric: it was defined in a 2013 peer-reviewed paper applied at Oak Ridge National Laboratory and is independent of any supplier (Energy Efficient HPC Working Group; see Uptime Institute on metric adoption, 2025).

Where heat reuse is the value driver, the design becomes a heat pump. Fenagy's installation in Kajaani, Finland, uses isobutane (R600a) and propane (R290) heat pumps to turn 13.5 MW of IT load into roughly 18 MW of heat for a district network serving about 3,500 households, at heating COPs of 4.2 to 5.0, and won an open tender against HFC and HFO options on price, COP, and technical design (Fenagy, via ATMOsphere). That is a refrigerant chosen by the heat resource, not the heat load.

Regulation tightens the funnel further. From 1 January 2027, EU rules prohibit stationary chillers above 12 kW that contain F-gases with a GWP of 750 or more, except where safety requires otherwise (European Commission). For many EU sites that removes a large part of the synthetic catalogue from new builds and pushes selection toward R717, R290, R744, or low-GWP alternatives.

The case against assuming naturals always win

The resource map does not always end at a natural refrigerant. Megawatt-scale propane on an urban rooftop carries a fire load that some operators will not accept; Carel's Enrico Boscaro, who chairs the Eurovent IT cooling task force, has flagged exactly this concern and expects many new US entrants to default to R32 (Carel; Eurovent). Vertiv has found in operator surveys that water availability ranks far below electricity as a stated siting worry, which complicates the assumption that water scarcity will universally drive design (Vertiv, cited in AWWA). Stulz is pursuing an A2L and low-GWP synthetic path with refrigerants such as R454C and R1234ze rather than committing to naturals, and Danfoss frames the F-gas phase-down as a portfolio question across both camps (Stulz; Danfoss). The honest framework treats the natural refrigerant as the frequent answer where power, water, or heat reuse leads, not as a foregone conclusion.

What comes next

This analysis maps the logic from the outside, using public data and disclosed projects. The second article in this series will test the framework against practice: how operators and designers actually weigh power, water, and heat reuse when they specify a system, where the resource-first logic holds, and where it breaks down against codes, insurance, procurement metrics, and unfamiliarity with natural refrigerants. The aim is to move from what the data implies to what the people making these decisions are seeing on the ground.

We are inviting industry voices to contribute on the record. We are particularly interested in data center operators and colocation providers; design and engineering consultants; neutral analysts and institutes working on efficiency and resource metrics; refrigerant and equipment manufacturers across both the natural and synthetic camps; and regulators and associations shaping the mandates.

For a sense of the format, our recent market analysis Beyond Refrigeration: How CO2 Systems Are Becoming the Energy Hub of Modern Food Retail drew on ten operators, manufacturers, and independent specialists across Europe and North America, each quoted on the record with their own data.

To take part, email the editorial team at info@refindustry.com or reach the editor-in-chief, Sergei Mukminov, directly on LinkedIn.

Sources

Primary sources

- Lawrence Berkeley National Laboratory, Queued Up: 2025 Edition (interconnection queue, ~5-year wait, ~2,290 GW): https://emp.lbl.gov/queues

- US DOE / LBNL, 2024 United States Data Center Energy Usage Report (electricity share, water consumption): https://eta-publications.lbl.gov/sites/default/files/2024-12/lbnl-2024-united-states-data-center-ene...

- Grid Strategies, National Load Growth Report 2025 (+166 GW to 2030): https://gridstrategiesllc.com/wp-content/uploads/Grid-Strategies-National-Load-Growth-Report-2025.pd...

- Gallup, Americans Oppose AI Data Centers in Their Area (March 2026): https://news.gallup.com/poll/709772/americans-oppose-data-centers-area.aspx

- European Commission, F-gas Regulation 2024/573, air conditioning and chillers: https://climate.ec.europa.eu/eu-action/fluorinated-greenhouse-gases/climate-friendly-alternatives-f-...

- Build.inc, Data Center Cooling in 2026 (dating of the ~2023 shift): https://build.inc/insights/data-center-cooling-technology-2026

- Energy Efficient HPC Working Group, TUE metric (ORNL, 2013), hosted by LBNL: https://datacenters.lbl.gov/sites/default/files/isc13_tuepaper.pdf

Secondary sources

- ATMOsphere, Clean Cooling for Data Centers (market figures and the BAC, Zudek, Secon/Penta Infra, Fenagy cases; a natural-refrigerant market accelerator, figures attributed to named companies; full report and per-company deep dives): https://atmosphere.cool/clean-cooling-for-data-centers-report/

- Bloomberg via Sightline Climate, US data center delays 2026 (reported): https://www.techradar.com/pro/if-one-piece-of-your-supply-chain-is-delayed-then-your-whole-project-c...

- Ecolab, Smart Water Conservation for Future-Ready Data Centers (heat capacity and transfer figures): https://www.ecolab.com/news/2025/09/smart-water-conservation-for-future-ready-data-centers

- AWWA, Cooling the Cloud (water projection to 2028): https://www.awwa.org/wp-content/uploads/AWWA-Cooling-the-Cloud-Water-Utilities-in-a-Data-Driver-Worl...

- Environmental Law Institute, Data Centers and Water Fact Sheet (January 2026): https://www.eli.org/sites/default/files/files-pdf/Data%20Centers%20and%20Water%20Fact%20Sheet%20ELI%...

- Data Center Watch, Q2 2025 update (blocked and delayed investment): https://www.datacenterwatch.org/q22025

- White & Case, German Energy Efficiency Act requirements for data centers: https://www.whitecase.com/insight-alert/data-center-requirements-under-new-german-energy-efficiency-...

- Orrick, German EnEfG draft amendment (April 2026, proposed PUE relaxation): https://www.orrick.com/en/Insights/2026/04/German-Energy-Efficiency-Act-Draft-Amendment-What-it-mean...

- Cundall, Why Germany's Energy Efficiency Act makes waste heat recovery a national priority: https://www.cundall.com/ideas/blog/why-germanys-energy-efficiency-act-makes-waste-heat-recovery-a-na...

- Goldman Sachs Research, behind-the-meter and fuel cells for data centers: https://www.goldmansachs.com/insights/articles/fuel-cells-could-help-meet-the-power-demand-from-data...

- Distilled Earth on Cleanview behind-the-meter data: https://www.distilled.earth/p/bypassing-the-grid-how-data-centers

- Uptime Institute on data center metrics and PUE limits (2025): https://journal.uptimeinstitute.com/is-this-the-data-center-metric-for-the-2030s/

- Eurovent, refrigerants position: https://www.eurovent.eu/issues/refrigerants/

- Stulz, adapting to EU F-gas with low-GWP solutions: https://www.stulz.com/newsroom/detail/f-gas-regulation/

- Danfoss, data center policies in the EU: https://www.danfoss.com/en/markets/buildings-commercial/shared/data-centers/data-center-policies-in-...