The global industrial refrigeration service market size was valued at $3.8 billion in 2020, and is projected to reach $7.1 billion by 2032, growing at a CAGR of 4.9% from 2023 to 2032. Industrial refrigeration services refer to all the services pertaining to industrial refrigeration systems.

Market Dynamics

Industrial refrigeration services are vital systems in many industries, as they are used for keeping various temperature-sensitive goods from food and beverages, pharmaceuticals, chemicals, and other industries. In the past few decades, the growth witnessed by these industries has been immense. For example, between 2011 and 2021, the total production sale of chemicals in the European Union increased from $746.7 billion in terms of value, reaching a peak of $909 billion in 2021. Medical-related chemicals accounted for the highest share. Moreover, according to the Germany Trade & Invest (GTAI), the food and beverage industry generated a production value of around $230 billion in 2022. In addition, various industries such as petrochemicals, chemicals, pharmaceuticals, and other industries use refrigeration systems to extract heat from their process machinery to prevent them from overheating. In recent times, the demand for petrochemicals such as oil and gas has increased substantially. For instance, according to the International Energy Agency, global oil demand is expected to rise by 6% between 2022 and 2028 to reach 105.7 million barrels per day. This will have a positive impact on the petrochemical industry, which is expected to eventually benefit the industrial refrigeration services market.

Both, original equipment manufacturers (OEMs) and consumers, profit from third-party services for industrial refrigeration systems. Third-party service providers offer extensive knowledge and experience in design, installation, maintenance, and repair of refrigeration systems. Customers benefit from the expertise of professionals who are familiar with the complexity of refrigeration technology. However, OEMs may focus their own resources on essential business operations and strategic objectives by outsourcing refrigeration services. This results in increased operational efficiency and the capacity to direct resources toward areas that promote development and innovation.

However, the fluctuating cost of raw materials used for manufacturing industrial refrigeration equipment is expected to restrain the market growth. Even if the manufacturer does not increase the price, it is expected to affect the profitability of the company involved in making industrial refrigeration equipment and their components. In addition, the services pertaining to industrial refrigeration are expensive as the technicians hold extensive expertise, which comes with a lot of money and time. Thus, expensive services are expected to restrain the industrial refrigeration service market growth.

Furthermore, the World Trade Organisation estimated that the overall value of global goods trade, including food, drinks, and agricultural products, would be $25.3 trillion in 2022, rising by 1.7% in 2023 and 3.2% in 2024. Furthermore, according to PwC 2021 research, expenditure on food goods is predicted to increase by 2030. This will generate demand for a better and larger cold chain sector globally. Developing countries especially, are witnessing increased growth in the cold-chain industry. For instance, in October 2022, the Guangzhou Nansha International Logistics Center began its operation of cold chain import business. Guangzhou Nansha International Logistics Center is the largest single cold storage in China. Moreover, in December 2022, a 5,000 metric ton capacity cold-storage facility began its operation in the Assam state of India.

The industrial refrigeration services market witnesses various obstructions in its regular operations due to the COVID-19 pandemic and inflation. Earlier, the global lockdowns resulted in reduced industrial activities, eventually leading to reduced demand for industrial refrigeration services from various sectors such as food and beverages, pharmaceuticals, petrochemicals, and others. However, COVID-19 has subsided, and the major manufacturers in 2023 are performing well. Also, rise in global inflation is a new major factor hampering the entire industry. The inflation is a result of the war between Ukraine and Russia and a few long-term impacts of the coronavirus pandemic. This has introduced unpredictability in the prices of raw materials used for manufacturing industrial refrigeration equipment. In addition, the cost of oil & gas has also increased substantially, and many countries; especially, the countries in Europe, Latin America, North America, and Sub-Saharan Africa experience severe negative impacts on industrial production of food and beverages, pharmaceuticals, and other industries, including the production of industrial refrigeration equipment. However, India and China are performing relatively well, and the production of industrial produce is witnessing rise unlike other countries; prompting increase in demand for industrial refrigeration equipment and services and positively affecting the industrial refrigeration service market outlook in these countries for ner future.

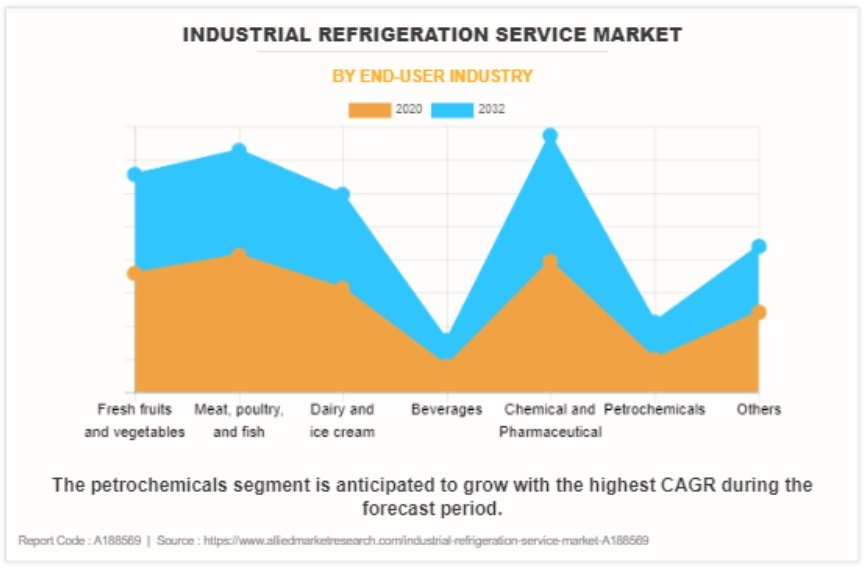

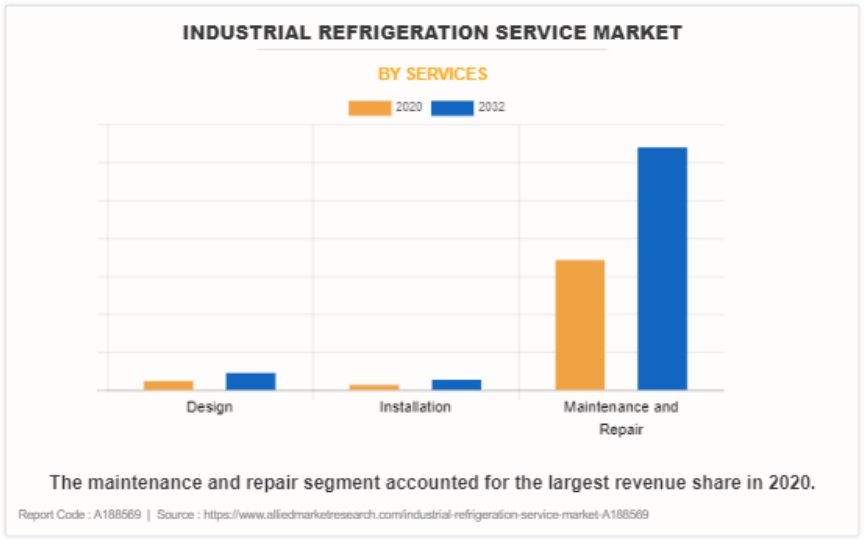

Segmental Overview

The industrial refrigeration services market is segmented on the basis of services, end-user industry, and region. By service, the market is divided into design, installation, and maintenance and repair. By end-user industry, the market is categorized into fresh fruits and vegetables, meat, poultry, and fish, dairy and ice cream, beverages, chemical and pharmaceutical, petrochemicals, and others. Region-wise, it is analyzed across North America (U.S., Canada, and Mexico), Europe (Germany, France, Italy, UK, Spain, Netherlands, Belgium, Poland, and rest of Europe), Asia-Pacific (China, India, Japan, South Korea, and rest of Asia-Pacific), and LAMEA (Latin America, Middle East, and Africa).

Read More