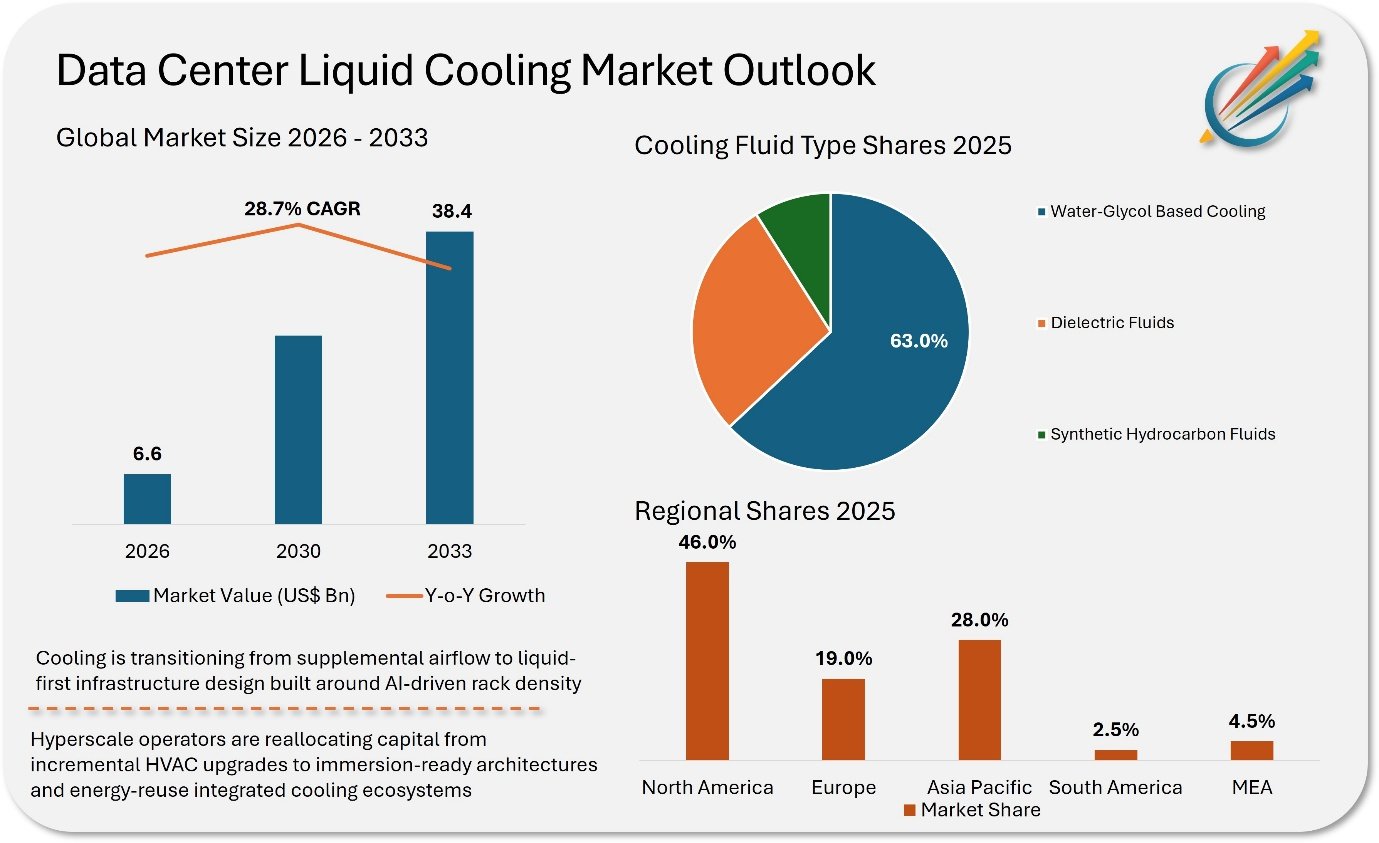

The data center liquid cooling market is projected to grow from USD 6.6 billion in 2026 to USD 38.4 billion by 2033, representing a 28.7% CAGR over the period, according to Market Minds Advisory. The report links growth to rapid expansion in AI and high-performance computing workloads and continued hyperscale data center build-outs, where it says traditional air-cooling systems are increasingly unable to manage escalating rack densities. It adds that direct-to-chip and immersion cooling technologies are moving into mainstream deployments as energy-efficiency and sustainability targets intensify.

The report states that AI training clusters are exceeding 30–50 kW per rack (approx. 102,000–171,000 BTU/h), and that next-generation GPUs are pushing thermal thresholds. It also says chipmakers such as NVIDIA and AMD are releasing processors with thermal design power exceeding 700 W (approx. 2,390 BTU/h), prompting operators to retrofit existing infrastructure or develop “greenfield” liquid-first facilities, with a focus on power usage effectiveness reduction and carbon footprint optimization. Market Minds Advisory also points to regulatory pressure around energy efficiency and water consumption as a factor supporting adoption.

Among its key takeaways, the report says direct-to-chip cooling is a key revenue contributor due to easier integration into existing racks, while immersion cooling is expected to be the fastest-growing segment due to heat rejection performance for hyperscale AI deployments. It also highlights rising adoption of rear-door heat exchangers as a bridge technology for hybrid environments, and growing demand for dielectric fluids, including “bio-synthetic and sustainable variants,” which it says can replace PFAS.

On market dynamics, Market Minds Advisory describes modular and retrofit-friendly systems as an opportunity area, including hybrid approaches that combine air and liquid cooling without a full facility redesign. At the same time, it cites high initial capital expenditure as a constraint, pointing to facility redesign, plumbing integration, specialized containment, and concerns around coolant compatibility, leak management, and maintenance training.

Regionally, the report identifies North America as the primary investment hotspot and says the United States accounts for the majority share due to deployments of large-scale AI data centres. It also describes growth in Asia-Pacific, including China and Singapore, and notes Europe’s focus on heat recovery aligned with environmental directives such as the EU Green Deal.

In the competitive landscape section, the report describes increased partnerships between cooling solution providers, chip manufacturers, and hyperscale operators, including “chip-to-chiller integration” and co-development agreements with server OEMs. It lists key players including Asetek Inc. A/S, CoolIT Systems, Submer, Asperitas, Iceotope, LiquidStack, Green Revolution Cooling Inc., Schneider Electric, Vertiv Group Corp., Rittal GmbH & Co. KG, STULZ GMBH, Eaton, Hewlett Packard Enterprise, Alfa Laval, Lenovo, DCX Liquid Cooling Systems, Huawei, Fujitsu, Delta Electronics, and Airedale / Modine.

Source