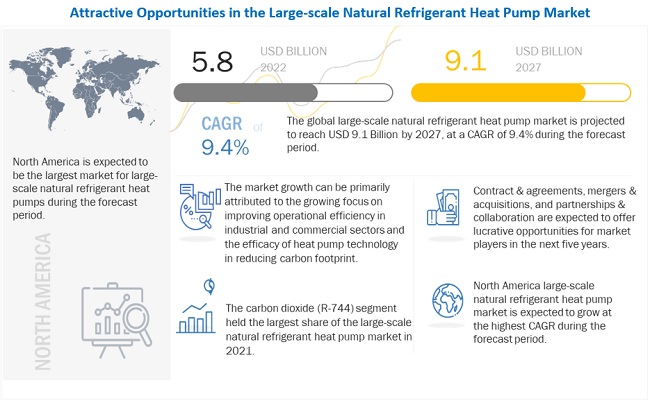

The global large-scale natural refrigerant heat pump market is projected to reach USD 9.1 billion by 2027 from an estimated market size of USD 5.8 billion in 2022, at a CAGR of 9.4% during the forecast period. The factors driving the growth for large-scale natural refrigerant heat pump market is increasing visibility of contribution of heat pump technology in reducing carbon footprint.

COVID-19 Impact on the Large-scale natural refrigerant heat pump market

Both the service and manufacturing industries have been badly impacted by the COVID-19 pandemic. The global economy has slowed as most countries around the world have enacted statewide lockdowns to prevent the virus from spreading further. The epidemic, according to the World Bank, provoked a significant recession and is projected to have a long-term impact on the global economy. The disruption of the supply chain and a sharp drop in demand in the commercial and industrial sectors hampered the expansion of large-scale natural refrigerant heat pumps. The market fell as a result of the suspension of major building and renovation projects. However, the market showed early signs of recovery, aided by government financial incentives to mitigate the impact of the pandemic..

Large-scale Natural Refrigerant Heat Pump Market Dynamics

Driver: Increasing visibility of contribution of heat pump technology in reducing carbon footprint

Heating is the largest energy end use, accounting for almost half of the total energy consumption in most countries. Thus, major economies across the world aim to reduce their dependency on non-renewable energy sources and are gradually inclining toward renewable energy sources to restrict the emission of greenhouse gases.

Heat pump technology is a promising solution for lowering greenhouse gas emissions. Different large-scale heat pumps, such as closed-cycle mechanical heat pumps, open-cycle mechanical vapor compression (MVC) heat pumps, open-cycle thermocompression heat pumps, and closed-cycle absorption heat pumps, offer an energy-efficient approach to heating and cooling in commercial and industrial applications. The heat pump is often regarded as a renewable energy technology when used in heating, ventilation, and air conditioning (HVAC) systems.

With a coefficient of performance (COP) of 3, large-scale heat pumps are expected to produce 520 TWh (terawatt-hours) per year. As a result of the increase, they will be able to better utilize alternative heat sources such as ground-source thermal heat and waste heat from data centres. They can use intermittent renewable electricity at the same time. Growing visibility regarding the efficacy of large-scale natural refrigerant heat pumps in reducing carbon footprint has led to an increase in the adoption of these systems across both industrial and commercial sectors.

Restraint: Lack of awareness regarding benefits of heat pumps and heat pump standards among system vendors

A heat pump is a technically complex equipment. The awareness regarding the energy efficiency, cost efficiency, and environmental benefits associated with heat pumps, as well as technical know-how, are limited among various end users.

According to a research published by the United Nations Environment Program, contractors are unaware of standards and certifications such as those issued by the International Organization for Standardization (ISO). Furthermore, there is a scarcity of best practise examples for large-scale natural refrigerant heat pump applications, which limits market growth.Besides, the classification of heat pumps by industries and certain public awareness websites are perplexing for the general public

Opportunities: Imposition of carbon tax in multiple countries

Enabling heat pump technologies compete with gas for heat supply in the European energy market will require more balanced taxation levels between electricity and gas. According to the European Heat Pump Association (EHPA), electricity taxes and levies in Europe are currently unjustifiably higher than those applied to gas and other fossil fuels, resulting in higher heat pump operating costs.

Sweden has experienced a fall of 2.1% in household energy use since the introduction of the carbon tax, as well as the phase-out of fuel oil, which was replaced up to 75% by district heating and 25% by heat pumps. Consumer prices for electricity in the UK are five times higher than for gas, which hinders the adoption of electric heat pumps. To make matters worse, climate and social taxes account for 23% of the electricity bill. European countries are moving more quickly to phase out fossil fuels and decarbonize their heating sectors because carbon pricing can close the price gap between renewable and fossil fuel-based technologies. The combined use of heat pumps and rooftop photo generation may be boosted in Europe by replacing current subsidies with a carbon tax policy and reduced electricity taxes.

Challenges: Availability of low-cost fossil energy-based alternative technologies

While fossil fuels will meet more than 60% of global heat demand in the buildings sector in coming years, the recent rebound in oil and gas prices has resurrected the subject of renewable space and water heating technologies' cost-competitiveness. Initial investment costs, variable running expenses, fixed operating and maintenance costs, and the presence of financial and economic incentives or disincentives all play a role in the cost-competitiveness of heating systems. Conventional heating systems, such as boilers, are driven by fossil energy, which is comparatively cheaper. The operation and associated installation costs are also low when compared with the heat pump technology. This challenges the market growth.

The high upfront cost of renewable technology can create financing barriers for households, in addition to hurting overall cost-competitiveness. Investment grants, rebates, fiscal incentives, and lending schemes are all examples of policies that can help overcome these obstacles. Policies that encourage building energy efficiency can also help with the shift to lower-temperature distribution systems.

The Carbon dioxide (R744) natural refrigerant is expected to be the largest segment of the large-scale natural refrigerant heat pump market, by natural refrigerants, during the forecast period

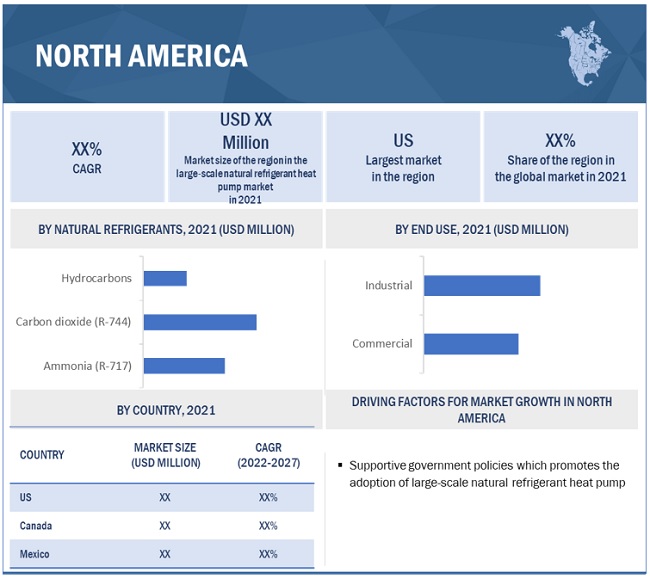

The large-scale natural refrigerant heat pump market, by natural refrigerants, is segmented into ammonia (R-717), carbon dioxide (R-744), hydrocarbons, and other refrigerants. The carbon dioxide (R-744) segment holds the largest share in the large-scale natural refrigerant heat pump market, followed by ammonia (R-717). The carbon dioxide (R-744) refrigerant is non toxic, non flammable and can be produced onsite which is expected to drive the carbon dioxide (R-744) refrigerant segment of the large-scale natural refrigerant heat pump market during the forecast period.

The 20-200 kW is expected to be the largest contributor to the large-scale natural refrigerant heat pump market, by capacity, during the forecast period

The large-scale natural refrigerant heat pump market, by rated capacity, is segmented into up to 20–200 kW, 200–500 kW, 500–1,000 kW, and above 1,000 kW. The 20–200 kW capacity segment accounted for a 42.4% share of the large-scale natural refrigerant heat pump market in 2021. The major advantages, suitability for light commercial and small industrial activity is expected to drive the 20-200 kW segment, which consequently increases the demand for large-scale natural refrigerant heat pump market during the forecast period.

The industrial segment is expected to be the fastest-growing market, by end use, during the forecast period

The large-scale natural refrigerant heat pump market, by end use, is segmented into commercial, and industrial. The industrial segment accounted for the largest share of 56.2% of the large-scale natural refrigerant heat pump market in 2021. Growing focus to increase the operational efficiency in the industrial activity is driving the industrial segment, hence, increase the demand of large-scale natural refrigerant heat pump in the coming years

North America is expected to dominate the global large-scale natural refrigerant heat pump market

The North America region is estimated to be the largest market for the large-scale natural refrigerant heat pump market, followed by Asia Pacific. The North America region is projected to be the fastest-growing market during the forecast period. The growth of the North America large-scale natural refrigerant heat pump market is expected to be driven by supportive policies implemented by the government for promotion large-scale natural refrigerant heat pump.

Key Market Players

The major players in the large-scale natural refrigerant heat pump market are Siemens Energy (Germany), Johnson Controls (Ireland), Emerson Electric Co. (US), GEA Group Aktiengesellschaft (Germany), and Mitsubishi Electric Corporation (Japan). Between 2017 and 2021, the companies adopted growth strategies such as contracts & agreements, investments & expansions, partnerships, collaborations, alliances & joint ventures to capture a larger share of the large-scale natural refrigerant heat pump market.

Read More