The dynamic in the UK has changed significantly since the pandemic, where it was still considered a commercially driven market, now the majority of multi-splits are sold into domestic. Single-splits remain mostly commercially driven, but here too the share of domestic has increased significantly.

Many products saw a recovery in sales in 2021, such as gas & oil boiler markets. This was more due to the release of delayed projects stalled in 2020 than any genuine growth. Some products, such as electric boilers and hydronic heat pumps, continued to increase in 2020 and into 2021. The drive towards electric heating was already increasing prior to the latest rise in utility prices. These two markets are expected to pick up more momentum in 2022, as other products also start to see some traction pushed by the trend towards net zero.

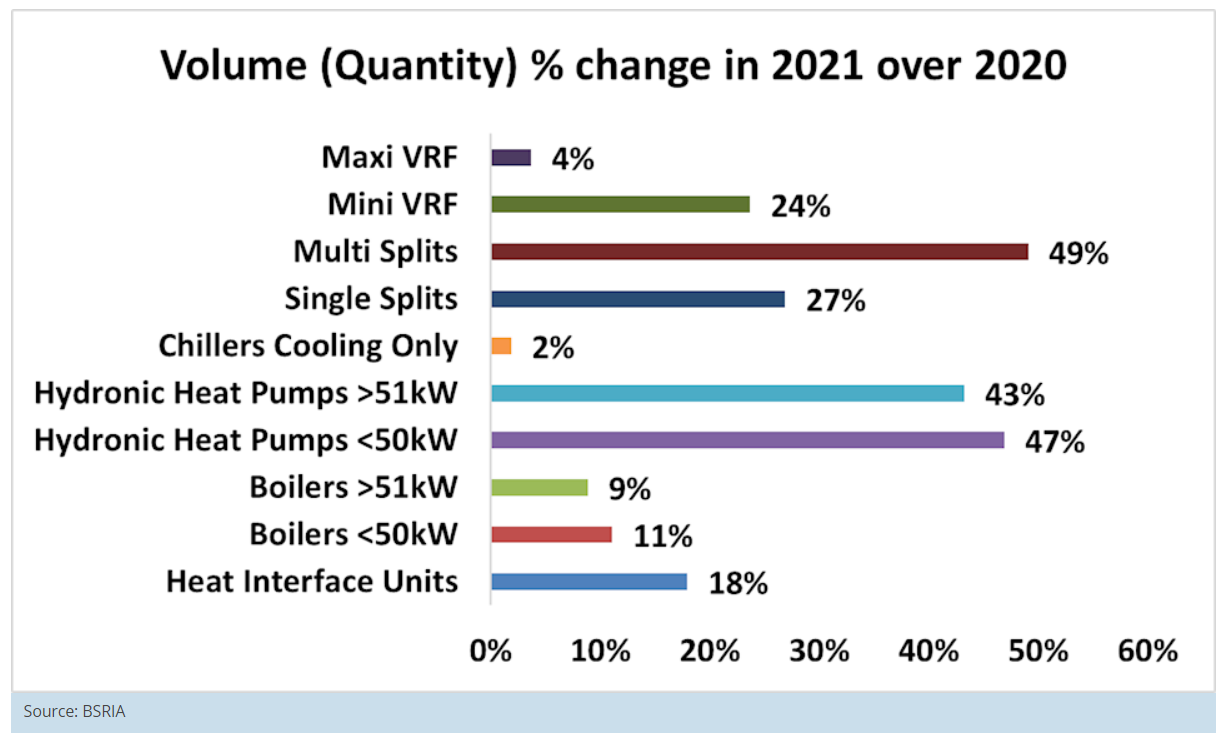

The Heat Interface Unit market is expanding, driven in part by the heat network initiative & the London Plan. Companies such as Ideal are investing in their own product range instead of using a 3rd party supplier. Compared with the gas & oil boiler markets, it is seen as having better growth prospects.

Electric boiler sales are increasing for domestic applications. These boilers are sold in small new build flats, where the hot water demand is higher than the heating load.

The release of CP1 CIBSE Guide Heat networks in December 2020 gives guidance on how to design systems with hydronic heat pumps working in parallel with an electric boiler. This has driven an increase in sales for large capacity (> 50KW) electric boilers for commercial applications, albeit from a low base, and has resulted in one or two brands entering the market. It is a growing market with limited competition, so offers good returns on margins.

Hydronic heat pumps are set to grow for domestic and commercial applications, as they are used to replace gas boilers mainly in new builds. Sales of heat pumps for new build domestic will rise significantly once the pending future homes standard is implemented in 2025. Housebuilders, on the other hand, remain cautious and are ramping up completions and slowing down starts.

The Ground source Heat pump market <50kW started to stall in 2021 as it was driven by the non-domestic RHI scheme, which closed in March 2021. It is possible the GSHP <50kW could fall in 2022, as some sales made for detached houses were driven by the domestic RHI scheme, which also closed in March 2022. The boiler replacement scheme is thought to benefit air source heat pumps for domestic applications, rather than ground source. This is because a grant of £5000 is offered for installing an air source heat pump, which makes the overall cost comparable to the cost of fitting a gas boiler. However, for ground source installations, whilst a higher grant of £6,000 is offered, the resulting cost is still much higher than fitting a gas boiler.

The drive towards low-carbon technologies has seen hydronic heat pumps >50kW take more share of the chiller market. For commercial applications, most companies are now reporting seeing predominantly air source heat pumps recorded on tenders. In fact, it was the air source market which saw the growth in 2021. Sales of water sourced 20KW+ fell over 2020. The main driver for heat pumps >50kW is the Salix funding scheme, which provides grants for the public sector. Private sector markets are driven by the London plan and net zero.

Hydronic heat pumps sales have grown, and so have air-to air-heat pumps. Single & multi split sales have continued to increase

Mini-VRF still has a sizeable number of sales made for high value residential in London, though sales for this application have declined recently. Much of the maxi-VRF market has been driven by refurbishment and the need for better energy efficiency and indoor air quality. But also, there is a push towards hydro kits which is now starting to drive maxi-VRF sales. These kits comprise a heat exchanger that transfers the heat from the refrigerant pipework to hydronic, which in turn provides underfloor heating or sanitary hot water

Demand for HVAC equipment remains high, at least in the short term. Lead times are extended due to shortage of components, so HVAC customers are adjusting to this by ordering much earlier and distributors are increasing their stock levels. Last year it was semi-conductors in short supply, which affected some brands more than others. This year it is wiring looms and EC motor fans. The Ukraine war has hampered production of wiring looms.

Questions remain whether the UK economy will enter a period of recession by the end of the year. Inflation continues to rise; transport fuel prices remain at an all-time high. Utility bills are expected to rise further in the autumn. However, Oxford Economics holds the view that consumer spending will slow, but not plunge, mainly due to high savings rates, thus it is too early to say if the UK economy will see a recession.